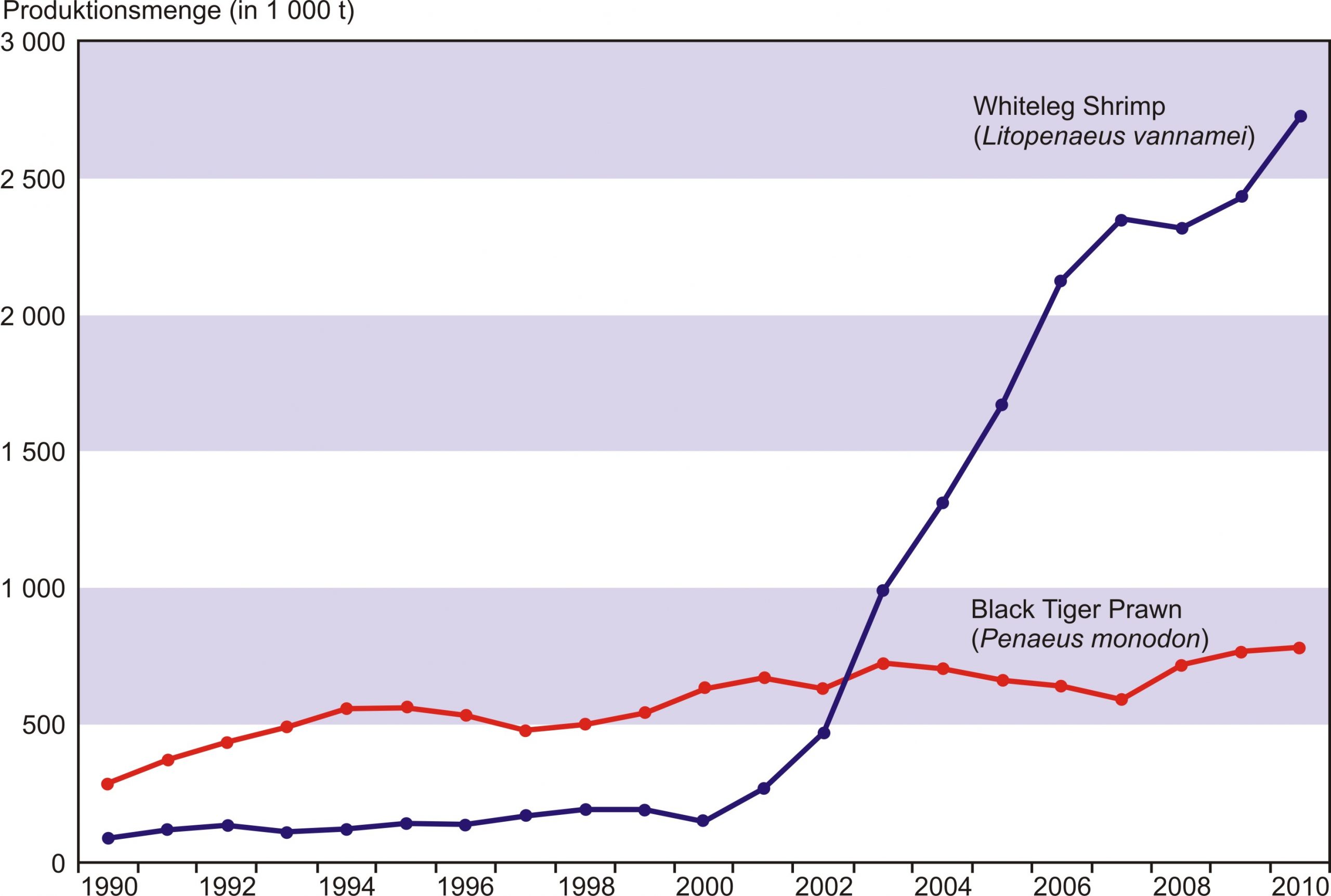

More than 2.72 million tonnes of white shrimp (Litopenaeus vannamei) were produced in aquaculture in 2010.

When a female shrimp that had been caught in the wild spawned for the first time in a test facility in Florida in 1973 the farming of Whiteleg Shrimp (Litopenaeus vannamei), usually known simply as white shrimp, began. It has been an unprecedented success story, for today this species is the most produced shrimp in the world’s shrimp farms. Production is stable and brings forth such large quantities that supply sometimes even exceeds demand.

During the last four decades we have seen rapid growth in aquaculture production of white shrimp. They were first hatched and reared in1973 and since 2003 white shrimp has been the most produced shrimp species throughout the world’s farming facilities. An amazing triumph for this little shrimp which originally comes from the coastal waters between Mexico and Peru in the East Pacific where temperatures of above 20°C prevail all the year round. Up to the 1990s white shrimp were only produced in Latin America, mainly through extensive farming in ponds. Thanks to selective genetic breeding it was soon possible to improve the economically significant performance parameters of the shrimps, and the life cycle of white shrimp in aquaculture was finally closed fully. This made the farms independent of wild parent shrimps and natural stocking because the necessary postlarvae could now be produced in hatcheries. The constant supply of high-quality stocking material to the farms is one of the most important prerequisites for meeting demand. The real breakthrough came, however, when in the 1990s experts succeeded in Hawaii in producing pathogen free (SPF) and pathogen resistant (SPR) L. vannamei lines. These developments made shrimp farming overall more stable and vannamei highly attractive for shrimp farmers in Asia, too. A large number of farms in Asia that had previously produced black tigers switched to white shrimp. After a decade ago more vannamei were produced in worldwide aquaculture than monodon the white shrimp became the most produced shrimp in global aquaculture.

Although Pacific white shrimp (Litopenaeus vannamei) grows to a maximum length of 23 cm and is thus one third smaller than the giant tiger prawn (Penaeus monodon) which can grow to a length of up to 36 cm white shrimp has a higher yield: 66 to 68 per cent more shrimp meat from Vannamei compared to 62 per cent from monodon. White shrimps also tolerate low salinities and can even survive in fresh water. This means that vannamei offers more possibilities for farm locations than black tiger which can only be farmed under marine conditions. The biggest advantage, however, is the availability of SPF and SPR postlarvae because this drastically reduces the need for chemicals and medication. The development of pathogen resistant and pathogen free lines was only possible after the closing of the vannamei life cycle in aquaculture. For monodon this has proved possible only in individual cases. Monodon postlarvae are in the meantime mainly produced in hatcheries, too, but a lot of the parent shrimps are still taken from wild catches. This constitutes a further high risk that the parent shrimps will pass on to their offspring diseases which can then be brought into the farms.

In the past it was often chance occurrences or hardly controllable diseases that decided the fate of shrimp farming facilities. Thanks to the progress made with vannamei and the farming and technological achievements with this species shrimp farming has become less susceptible to disease, more constant, safer and ultimately also more efficient and more planable. Production is in the meantime so stable that it actually endangers its own commercial success. It sometimes happens that production from shrimp farming is in excess of actual demand.

Important farming countries trying to cut back shrimp production

At the end of the second half of 2012 it again became apparent that more shrimps were being produced worldwide than the potent markets can absorb. A considerable share of the products could only be sold at strongly reduced prices. The situation on this very special market is extremely complex. The interplay of demand and supply is rarely balanced which is why it constantly has to be readjusted. When demand rises this adjustment process presents no big problem since the short production cycles of shrimp allow relatively fast production increases: depending on the climatic zone two to three harvests a year are possible. The opposite case is much more difficult to tackle: it is not easy to reduce production once farming has really got going.

At the beginning of 2012 a lot of the forecasts were still relatively pessimistic. Vietnam, after China and Thailand in the meantime in third place in global shrimp aquaculture, reported considerable harvest losses. Virus epidemics such as NHP and IMNV had led to huge damages, first in the Mekong Delta and then later in the northern and central regions of the country. In some areas the shrimps developed a higher susceptibility to disease due to unusually strong fluctuations in day and night temperatures. Production losses meant that a lot of farming enterprises got into the red with the result that they were then often no longer allowed loans by the banks. In some cases farms produced so few shrimps that individual processing companies even had to import raw materials from abroad in order to fulfil their export obligations to their customers. To make matters worse, Japan, the most important export market for Vietnamese shrimps, authorised that shrimp products from India and Vietnam should be more strictly controlled. During routine controls they had come up against ethoxyquin residues in excess of the permitted 0.01 ppm. Ethoxyquin is a kind of antioxidant agent which is mixed with the feed as a means of protecting against spoilage under tropical climatic conditions.

Whilst in Vietnam production losses were rather the result of the conditions prevailing there, other producing countries intentionally tried in to cut back shrimp production in the second half of 2012. This was the case in Thailand and Indonesia, for example, because demand and prices remained weak. Indonesia’s government reduced its production targets for the shrimp farms to 300,000 t and additionally set up a promotion programme for supporting the marketing of shrimps on the domestic market. Thailand, after China the second biggest shrimp producer and at the same time the world’s most important export nation for shrimps, faces even bigger challenges. The intensive shrimp farms in Thailand operate under very high production standards and this leads to higher costs which in turn make the shrimps more expensive. This is a considerable competitive drawback, particularly when the economy in the target markets is slack and demand low. A support programme set up by the Thai government succeeded in stabilising ex-farm prices with support purchases but this is naturally only possible in the short term. Sales problems could even be exacerb

ated as shrimp production continues to rise worldwide and competition and price pressure are increasing. Of further concern for Thailand’s shrimp industry are the new GSP regulations for exports to the EU (GSP: Generalised System of Preferences). Should these take effect as planned in January 2014 it would make shrimps from Thailand even more expensive. Export duties for raw shrimps will rise by 4.2% to 12%, for cooked and cocktail shrimps by 7 to 20 per cent.

More and more farms in India are switching to Vannamei production

One reason for the current turbulences on the shrimp market is developments in India which had long held back from importing and producing vannamei shrimps because they felt that the risk of infection through diseases and ecological and social risks was hardly calculable. In the face of the production achievements made in particular in Thailand and Indonesia through the use of SPF and SPR shrimps India gave up its resistance a few years ago, also and particularly due to the fact that their traditional shrimp production which was mainly based on black tigers had fallen by 7.7% during the period from 2005 to 2009 when a lot of farms were hit by diseases. Following the success of initial attempts to farm vannamei on a 10,000 hectare pond area in the state of Andhra Pradesh white shrimp farming is now growing fast. More and more shrimp farmers are switching from farming monodon, whose production has allegedly already fallen by half, to vannamei. Official production figures speak of only 130,000 t vannamei but insiders estimate that the actual production volume is considerably higher, perhaps even double the official figure. Farms that do not produce for export are hardly registered and their production is – if at all – only recorded carelessly.

Domestic demand for shrimps on the Indian market is high, particularly for the smaller counts above 70 (HOSO per kg). Larger counts usually go into export. Some European countries have increased their imports from India, and the USA are also importing more than in the past. US imports from India rose by 59% to 48,100 t in 2011 compared to 2010. This hurts Thailand in particular since their export industry had traditionally supplied the US market. Compared to Indian shrimps Thai shrimps are about 10 to 20% more expensive which leads to considerable price pressure. A lot of exporters can currently only sell their products with hefty price reductions. Although the low-price vannamei shrimps at present only contribute about one third towards India’s shrimp exports (at the moment vannamei account for 35% of shrimp exports, monodon’s share has dropped from formerly 82 to 61 per cent) they are reaping record sales for the country’s seafood exporters. In the business year 2011/2012 India exported fish and seafood worth 3.5 billion USD, with shrimps accounting for nearly half, or 1.7bn USD. Although the export of Indian shrimps to Japan has become more difficult due to excessive ethoxyquin residues sales of farmed shrimps to South East Asia have more than doubled in volume terms, and even tripled in value terms. This success has whet appetite for more and the MPEDA, the authority responsible for promoting seafood exports, is hoping for an increase to 4.5bn USD for the current fiscal year.

This is to be made possible by increasing vannamei production and by extending and modernising the country’s processing facilities in order to be in a position to produce more value-added products for export. Frozen and storage capacities, in particular, are being expanded. Some producers are also investing in processing machines too, however, because wages in the seafood processing industry have risen fairly strongly by Indian standards. The success of Indian shrimps on the international markets is putting additional pressure on the country’s shrimp industry because the currently low demand and subsequent low price level is also a burden on India’s shrimp farms. Export-oriented companies, in particular, reported lower production figures for the second half of the year but sometimes the decreases are not caused by intentional reductions in production but more by the poor quality of the stocking material… The hatcheries are currently having difficulties coping with the massive growth in demand for vannamei postlarvae and even low-quality shrimps are quickly snatched up.

Euro problem in Europe affecting the shrimp market

After three relatively stable years in which demand and prices displayed neither strong rises nor falls the shrimp market suddenly collapsed in mid-2012. The price for black tigers (16/20) from Bangladesh that cost 12 to 13 USD/kg in June suddenly fell by two dollars within just one week. Although a lot of importers negotiated new prices and passed them on to their customers they were not able to sell all of their stocks. And even the low price level could not stimulate the sluggish demand lastingly.

The continuing euro crisis and the economic problems of some EU countries have caused demand in Europe to remain low. Consumer buying power has decreased and the weak euro makes imports more expensive. Under these conditions cheaper shrimps are more popular, for example from Bangladesh, which benefits from GSP, or from India. Thailand was able to assert its position as the most important supply country for the EU market but Bangladesh, which increased its exports to Europe by 35.7% and India, whose exports rose by 22.2%, benefited much more strongly from the current developments. Because customers mainly look at the price per kilogram when buying shrimps importers sooner choose smaller piece weights for vannamei shrimps under the present conditions. In Spain 60/80 counts are particularly popular and in France even smaller 80/100/kg shrimps. The usual stimulation of business at the end of the year failed to happen. It is hardly to be expected that the EU market will recover rapidly and find its way back to its usual strength under the present general economic conditions.

The fact that demand for shrimps in the UK remained almost stable is probably thanks to the Olympic Games in the summer of 2012 which livened up the market considerably. The German market also displayed only few changes. The effects of the euro crisis were to be seen most strongly in Spain where demand fell by one fifth in 2012. Although demand in Italy decreased to about the same extent the economic effects of the slump in demand are harsher in Spain because Spain is the biggest importer of shrimps from aquaculture in the EU.

Demand in the USA is also relatively low on account of the economic problems there and a lot of importers are waiting to see what happens. Although shrimps continue to be the most important seafood product consumption preferences have shifted. Whilst shrimps used mainly to be consumed in restaurants a lot of consumers now choose to eat them at home to save money. This improves the market chances for convenience products but exporters have mainly ordered non-processed frozen (head-on and head-off, raw or cooked) shrimps. It remains to be seen whether a better offer of value added shrimp products might succeed in stimulating demand again. Shrimp products that have undergone further processing have the advantage that in contrast to raw shrimps they are rarely subject

to anti-dumping penal duties. For value added products it is generally of no importance whether the products were produced using black tiger or white shrimp. The two species differ only slightly from a culinary point of view. However, consumers in the USA seem to be of a different opinion here, as a test of the Food Science and Human Nutrition Department at the University of Florida recently confirmed. According to this, vannamei are considerably more popular among American consumers than monodon. The Americans favour shrimps that have grown in water with a low salt content. Apparently their aroma, smell, appearance and texture are better then.

The shrimp market in Asia is at the moment fortunately less gloomy. Although the economy in China is no longer growing quite so dynamically as in previous years, demand is still very high. About three quarters of Chinese shrimp production is consumed within China itself. Demand is growing in other Asian countries, too, although not sufficiently strongly to offset the drop in demand in Europe and North America. In Japan, which buys about 80% of its shrimp imports from Asian countries, particularly Thailand, Indonesia, Vietnam, India and China, demand even rose in the first six months of 2012 by more than 2%. The ethoxyquin residues detected in Vietnamese and Indian shrimp imports have apparently hardly worried Japanese consumers or stopped them from buying – particularly since the favourable shrimp price is a convincing sales argument.

Experience has shown that consumers in Europe react much more sensitively to such occurrences. And this means that the EU regulations, maximum residue limits and import controls are accordingly severe, with the zero tolerance principle applying to some chemicals and antibiotics. The standards are equally high on all other important markets, whereby in the USA there is also a very strong focus on hygiene standards such as HACCP, as on flavour and sensory quality parameters.