Small scale vessels dominate in numbers, but amount to only 10% of the total tonnage of the Italian fleet.

Over the past few years, national seafood production has been steadily declining until 2013; in 2014, a slight increase in the quantity was recorded with a production of 325,000 tonnes of seafood. In terms of value, the negative trend continued also in 2014. This decline affects both marine fisheries and aquaculture. Molluscs are still the main product of the national aquaculture sector; the main harvest is of mussels (Mytilus galloprovincialis) and clams (Tapes philippinarum).

The overall production of marine fisheries in 2014 amounted to 177,000 tonnes and generated 813 million euro. In the last two years it lost an estimated 21,000 t and 121 million euro, a contraction that further weakened the sector and reduced its impact on the overall Italian economic scenario. In 2014, the trade deficit in the seafood sector amounted to 840,000 tonnes and 3,919 million euro. The deficit continues to rise due to a higher rise in imports over exports. Political instability affecting some countries bordering the Mediterranean and the challenging economic condition of several EU countries had an impact on the international seafood trade as well.

Apparent consumption – calculated as the difference between exports versus internal production and import – reached 1,166,000 tonnes in 2014. Even so, per capita consumption remains at minimal levels (18.55 €/kg in 2013 and 19,18 €/kg in 2014), far below the 20 €/kg recorded in 2005. The unfavourable state of the domestic economy and the related general decline in food consumption continues to affect seafood purchases.

| Figure 1: The macroeconomic scenario of the Italian seafood sector | ||||||

| Quantity, 000 tons | Value, € mln | |||||

| 2012 | 2013 | 2014 | 2012 | 2013 | 2014 | |

| Capture | 198 | 173 | 177 | 934 | 832 | 813 |

| Aquaculture | 191 | 141 | 149 | 465 | 393 | 365 |

| Total fishery production (a) | 389 | 314 | 325 | 1,399 | 1,225 | 1,178 |

| Import (b) | 903 | 919 | 976 | 4,207 | 4,240 | 4,507 |

| Export (b) | 117 | 126 | 136 | 501 | 548 | 588 |

| Apparent consumption | 1,175 | 1,107 | 1,166 | 5,105 | 4,917 | 5,097 |

| Per capita consumption (kg) | 19,78 | 18,55 | 19,18 |

Structural characteristic of the fishing fleet and trends in fishing effort

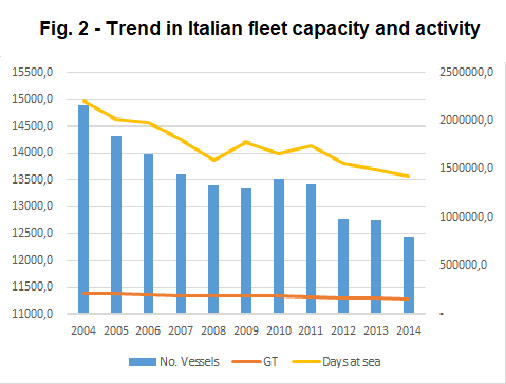

The national fleet registered in the Vessel Register, and operating as of December 2014, consists of 12,440 vessels accounting for a total tonnage of 156,876 GT and 999,758 kW. Trawlers account for most (62%) of the domestic tonnage; small-scale fishing vessels, though representing the largest number of units, only make up for 10% of the total tonnage. As for geographic distribution, the fleet still shows the same features that has always distinguished the Italian fleet: low concentrations – with the exceptions of Apulia and Sicily, both in terms of number of vessels and tonnage – and strong differences in specialization, in terms of productivity and profitability, between the Adriatic and Sicilian fisheries on the one hand, and the Thyrrenian fleet on the other.

A steady decline in fishi

ng activity characterize the Italian fleet: between 2008 and 2014 it fell by an average of 10%, dropping to 17% for bottom trawlers, 25% for hydraulic dredges and 6% for small scale vessels. This trend can only partly be attributed to an increase in fuel price, though this surely had an impact on the trend over the last three years. But more generally, the decline in fishing activity can be explained by a different organization of the fishing sector, where operators spontaneously adopted strategies to optimize time spent at sea, both for commercial reasons and in order to cut back on operation costs associated with fishing and landing activities.

The fishing capacity of the national fishing fleet is subject to adjustment plans that provide for the gradual withdrawal of units deployed for fishing activities. Over the last ten years, the fleet has been affected by a continuous decline in all technical parameters decreasing by 7% in number and by 14% in total tonnage (fig.2).

Fishery production in the Mediterranean sea

In 2014, the Italian fleet produced 176,778 tonnes of seafood generating 812,506 million euro. Results are down 2% in value since 2013, following the downward trend of the last few years, also characterized by a consistent downscaling of the sector (fig.3). In terms of quantity, in 2014, a slight increase has been recorded (+2%).

Several factors contributed to the fall in total captures and unitary productivity: changes in fishing zones, increased production costs, and a different composition of the catch, which targeted the most sought-after species on domestic and international markets affected by the economic crisis. The restrictions imposed by the Mediterranean Regulation 1967/2006 also had a direct effect on production: these involved mesh size, distance from the coast, minimum size of several species and the modifications in fishing activities they engendered. Finally, new control regulations and sanctions, which cover all operations from capture to sales, are bringing about changes in fishing operations, including the most traditional ones.

Prices at production

Over the last ten years, a constant decline in the unit value at production in spite of low supply has affected the fishery sector; a long-term analysis shows how, in spite of the considerable fluctuation of domestic production since 2004, prices always followed an independent trend, unrelated to trends in supply.

Amongst the most relevant species, anchovy saw in 2014 a decrease in price (-12%), while pilchards and clams remained stable. Red shrimps show a stable trend with a unit value of 18.50 €/kg in 2014; this trend is significant if compared with the domestic production that decreased in the last year (-20%). Such price increase is partly due to the growth in the domestic demand for high value fish products and partly to the adoption of initiatives aimed at qualifying products. To face the difficulties of the market, mainly due to the increasing competitiveness of foreign output, and in order to differentiate home products from foreign ones, Italian operators have set up initiatives and research aimed at making domestic products more easily identifiable. Even if such initiatives are still few, an ever-increasing number of operators adopted the system of certification as a means to mark out both fish production processes and final output. Such steps permitted good profit margins which mainly concerned sales of processed or fish farmed products. Still now, with some exceptions, the market of fresh fish is characterized by inadequate transparency, lack of information regarding the origins and the quality of products, high fragmentation of supply.

The profitability of the fishing sector

The fishing sector in 2014 continued to record considerably negative performances; the revenue produced by the fishing sector has consistently declined since 2008, a particularly bleak year for the industry. The added value produced by marine fishing in the last year was EUR461m, of which EUR235.76 million were allocated in salaries and the rest (EUR226m) represented the gross profits of the sector. The general contraction of the economy account in this sector, due to a rise in intermediate consumptions (goods) and a fall in revenue, had negative repercussions on labour cost: only 29% of revenue was allocated to crew payments in the last year. The rise in intermediate consumption was driven by the considerable increase in fuel price which rose from 0.59 €/lt in 2010 to 0,70 €/lt in 2014. The fuel costs per vessel increased and its weight on the income rose from 16% in 2004 to 27% in 2014 (fig.4).

In general, the negative trend shown by profits is more linked to the rise in costs, particularly variable costs, rather than a fall in revenue. In spite of lower quantities of products sold, the average commercial costs sustained by a single fishing vessel have slightly increased, while fixed costs remained stable. Since the last months of 2014, the fuel price show an inverse trend, with a steady decrease; in 2015, the average fuel price was about 0.54 €/lt. The decrease in fuel costs, that is the main cost item in fishery account, can have positive effects in the short period on the profitability of the fishery sector.

Rosaria Sabatella

NISEA, Fishery and Aquaculture Research Organisation

Via Irno, 11

84100 Salerno

Tel.: +39 089 79 57 75

r.sabatella@nisea.eu

www.nisea.eu

Data presented in this article is a summary of data collected within the Italian National Program on Fisheries Data Collection, Italian Ministry of agriculture, food and forestry policies, Mipaaf – EU Regulation n.199/2008